If you’re financing any major purchase through a retailer, that company doesn’t actually carry your loan. They are in the business of selling furniture, jewelry or home improvement products, but aren’t in the finance business.

But these companies know that they need to find a way to help tons of people get the financing in order to buy their products. That’s where many finance companies come in that you’ve never heard of. Yes, you can put the charge on your credit card, use your line of credit, or arrange a loan, but lots of people will simply get the store to be the middle person on getting the money arranged. That may be convenient, but it’s always much more expensive.

If you’re buying something at the Brick, for example, they’ll handle the application for credit with Flexity Financial. It’s owned by Curo Financial Technology. You need a pretty low credit score and can get approved for a credit line that’ll cover your furniture purchase. Or you can apply for the Brick Visa that’s done through Desjardins in Quebec. In the same way, the Lowe’s Consumer Card is issued by Synchrony Financial. It’s a US company with almost 70 million finance customers in everything from home improvements to vehicles, travel and home products.

A few years ago, financing started for air conditioners, furnaces, roofers and others. On the surface, that makes sense. Most people have no emergency savings, and are in no position to pay four, five or six thousand dollars for a new furnace or AC.

Plus, almost all of the companies in these industries are small or medium local businesses. They’d love to sell you a new furnace, but YOU need to have the money or get the financing done first. In came two or three finance companies who specialize in big ticket items for your home. If you look at most heating and air conditioning companies’ websites, they’ll have a link right on there to one of these finance companies.

When you hear an ad that you can have air conditioning or a new furnace for starting at only $39 a month – it’s not the contractor that’s financing it, it’s one of these companies.

Before you jump in, be super careful and read and understand every scrap of paper before signing it. Better yet, don’t do it. Find a way to find the money or, if need be, get a small line of credit or loan from your bank.

These finance companies will put a 12-15 year lien against your home. How can you have such a low payment? By stretching the time to forever! But forever means a staggering amount of interest, no matter what the rate. And they mirror all the mortgage lingo and rules: You’ll have a 12-15 year amortization. That’s the total length of the loan and a three or five-year term. That’s how long the initial rate is fixed before it’s changed. So two things: Most people see the word “term” and think that’s the total loan length. BIG mistake number one. And after five years, just like a mortgage, a $5,000 loan will still have a balance way over $4,000 because of the tiny payments and stretched term!

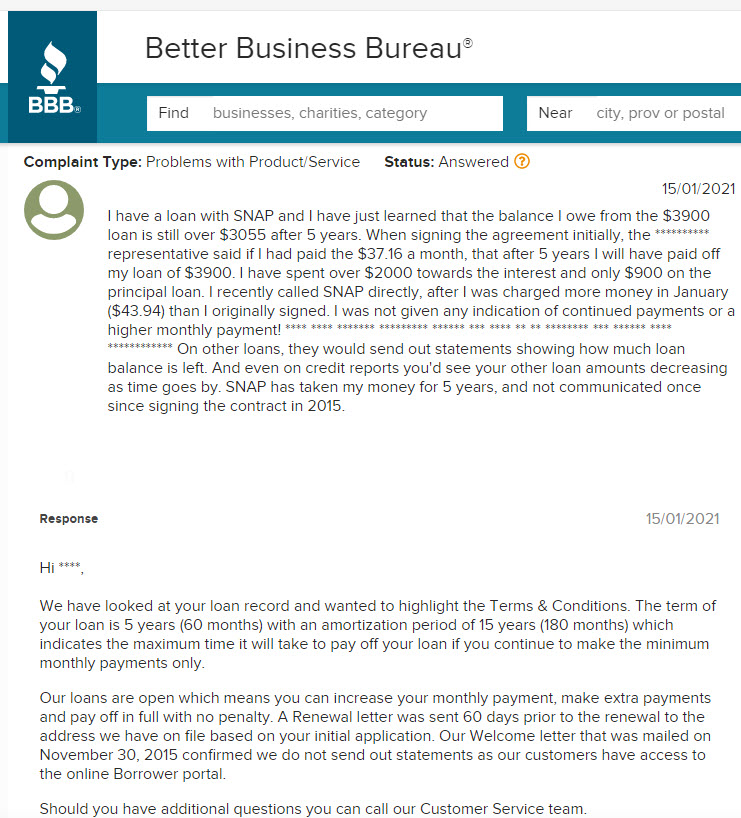

This person is a typical BBB complaint, but it’s not valid. All the information is in the signed loan documents. They thought the “term” of five years (and it’d be paid off) was the total amortization (15 years). They were surprised so little of their payments had gone to principal. Yup – five years of payments pretty much went mostly to interest. That’s the downside to a 15-year loan! They also complained that the payments went up 15%. Yup – after five years (in this case) they’ll move up the rate. A lot – in this case! Just like a mortgage – fixed for a while, then it’ll adjust.

Sure they can offer you a low rate because they have almost zero risk. Furniture type financing is 20 to 30% rates because they don’t have any collateral. They can’t come repossess your three year old couch. Financing your furnace or AC puts a forever lien on your home. You might not pay, but they’ll just add massive fees and penalties and they will always get paid because it’s the same as a 2nd mortgage: You cannot sell your home unless this debt is paid in full.

Yes, the AC, new furnace or solar may be necessary, and may even increase your home value – but you can’t transfer the debt. You have to pay the balance in full before the sale can close.

Finally, all of these finance companies charge a rip-off admin fee and MAY have big penalties in the fine print. The last one my realtor friend saw was a $6,700 early payout penalty. His seller had no choice but to pay it or his home sale would have collapsed. The same applies to any solar installation that’s financed.

If you’re wanting a new or replacement AC unit this summer, you can either sweat the bad finance contract for over a decade or sweat in your home until you can come up with the money. The choice is yours – but it’s definitely buyer beware!

PS: A 50% higher interest rate for half the time is still way cheaper! $5,000 at 8% over 12 years vs. six years at 12% is over $700 less interest. But then, most people finance a vehicle for 8 years when their track record for trading is 4 or 5 years…and the average in Canada is 4 1/2 years…and all of them are surprised and shocked when they owe way more on the loan than the value of their vehicle…