Late fall, the rollout of Sleep Country Canada stores into select Walmart locations started in Quebec. They’ve now worked their way to Western Canada with locations in Saskatoon, Lethbridge, Calgary, Edmonton, and Duncan, BC.

The express stores are around 700 square feet and may replace the hair salon, optometrist/eye glasses, nail salon or other smaller “stores” to make room. Sleep Country has around 300 locations and simply wants to expand their customer reach. Walmart is certainly the place to do that, so it seems like a win-win for both companies.

Mattresses, along with jewelry, certainly have enough markup to make them profitable, even after paying Walmart. When furniture markup is around 300 to 400% (compared to less than 10% for electronics) and mattresses are significantly higher than that, make sure you shop around. For over a decade, a national retailers has had a billboard on a busy intersection in Edmonton advertising 50% mattress sales. That’s not a sale – its re-establishing a lower (but still) retail price. That’s taught me to believe: 50% off is actually full sticker price.

Consumer Report is a good place to start your research. They’ve done testing on everything from $1,000 to $3,000 mattresses and found very little difference when cutting them open and comparing coil count and padding. In their opinion, suggested retail pricing is pure fiction and fancy phrases and brand names don’t justify the additional cost. Feel free to test-sleep them for a few minutes and shop around. If you have a Costco card and are looking for a new mattress, January is the month Costco carries them (as in: check it out right now) since it’s only a seasonal in stock item.

If you’ve ever wanted an insight into what rich people do with their money, here it is. It’s a research report from Personal Capital of over 50 NBA players. In some ways, they’re not so different from you and me. In other ways, you definitely don’t want to emulate what they do!

The average income is around $45,000. THAT is roughly what the average NBA player SPENDS in a month! But then, the rookie entry salary in the league is $4.7 million. But let’s see what they spend that half a million on every year:

11% goes to clothing and shoes – their biggest trackable expense category.

9% is automotive – even though most of them likely get a free vehicle from a dealership in return for some endorsements.

8% is travel – after all, it’s a long off season, and they like to travel in style, and to 5-star hotels and resorts, which isn’t cheap.

Restaurants eat up 7% of their spending. That’s around $35,000 a year, which will get you some great meals, even if you’re picking up the tab for others in your group.

Sadly and surprisingly, 7% is also what they donate to charities. That’s kind of a puny percentage for an income of more than five million bucks if you ask me.

5% goes to a category called service charges and fees. It’s kind of obvious here that over $25,000 of fees means they’re really not very financially literate, and certainly don’t shop around at all.

The one place they do seem to want to save money is shopping at Walmart. Yes, the average NBA player shops there, too – to the tune of over $45,900 a year!

But here’s where you want to be very different than an NBA player: Over 78% of them go bankrupt within two years of retiring from pro basketball. We spend what we make – that is: we spend to the amount of our pay. That’s not a good idea for us middle class earners or millionaire income athletes.

Yes, there are stories of pro athletes who are incredibly great savers and literally don’t spend a dime of their salary. But for every one of them, there are dozens who crash and burn. Vin Baker made over $100 million in his career and last month started a job at Starbucks to support his four kids. For millionaires and ourselves: Spend what you want, but only AFTER at least 10% comes right off your check, or out of your account, to pay yourself first.

Part of our run-away inflation is that we’re going to restaurants again – a lot! But servers are making less money than ever while working harder, and it’s something you didn’t know.

While your only contact is pretty much your server, behind the scenes are bartenders, hostesses, bussers, runners, kitchen staff and others who you aren’t tipping. Since you’re not coming into the restaurant with a wad of five dollar bills to hand out, those staff still do get a part of your tip. Different restaurants do it in different ways, but the most common in the industry is called tip-out. It’s a tip distribution system that does get some of your tip money to those other staff who are instrumental in making the server look good and able to function. In most restaurants and chains, their indirect tips have increased in the last few months when the restaurant increased the tip-out amount to a range of six to eight percent.

To translate that into English: A server who rings out (collects) $1,000 during their shift pays the restaurant an additional 6 to 8% over and above that. So they’re responsible for turning over $1070.00 if we use 7% as a tip-out. The server has collected a bunch of credit card charges, some gift cards, some cash, and tips. At the end of the shift, the computer adds up all of the charges for food, drinks, etc. that were charged to his or her swipe card (account) to come up with the total amount plus the added ring out. Whatever is left over is their real tip income for the shift. The seven percent is then distributed to those bartenders, hostesses, bussers, runners and kitchen staff (depending on how the restaurant has the people and the distribution percentages set up).

Since that tip-out has increased, it’s decreased the servers income unless you make 20 percent the new 15! They’re sharing more – keeping less. A $1,000 total for a server may generate 15% tips…but not likely since some tip less, others don’t tip at all! But let’s use 15%: The server has collected $1,150 and pays the restaurant $1,000 and the 7%, or $1,070. That leaves $80, or an actual tip of 8%! On an average 20% tip (oh how servers wished that were the case) the actual take-home amount would be $200 in tips, less the 7% ring-out or $130 net (13% of the customer bills total). So now you know…and now you have to decide the next time you’re eating out!

Walmart somehow also seems to think 20 is the new 15. But that’s not a good thing in the retail business. Again, lots of products have gone up in price. But not 25%! Like Covid and the Russian invasion of Ukraine (see the story from last week) became reasons to lie or use as excuses, it makes me wonder if retailers aren’t using this time to move up their profit margins under the radar…

There are lots of examples, but here’s my most obvious one. Once a year I buy a new pair of the least expensive jeans I can find. They’re for outside work season from painting to kneeling on the garage floor, or in the yard, and don’t last more than a year before I replace them. For a few years, that’s been Walmarts’ $15 jeans. These cheapest jeans I can find are $20 this year. No way – no how – no chance I’m paying that. Has Walmart’s long-standing campaign of “roll-back” pricing turned to “roll-forward?” It isn’t the price of denim, or any improvement in quality, or that much increase in freight costs….I’m sure they can still fit a few hundred thousand into each container leaving China…. But, judging by the empty racks, I’m very much in the minority in not swallowing a 25% price hike. Sad but true…

Update 5/25/22: Costco now has their own jeans under their Kirkland line for $17. The material is really good quality, they fit well and come in a wide range of sizes including odd numbered ones. Since they don’t have change rooms, buy them, and go into the washroom to try them on. Then you can exchange or return before leaving the store.

Loyalty is always a two-way street when it comes to the brands and the products we buy.

With some of the insane (and unjustified) price increases so far this year, loyalty to any one product can shred your wallet. That’s entirely unnecessary when there are normally substitutes that are just as good! I would estimate that there must be almost a dozen items that I’ve changed since the start of the year because of price increases of over 25%. Sorry, that’s not inflation – that’s taking advantage of the “everything is going up” resigned attitude to stick it to me.

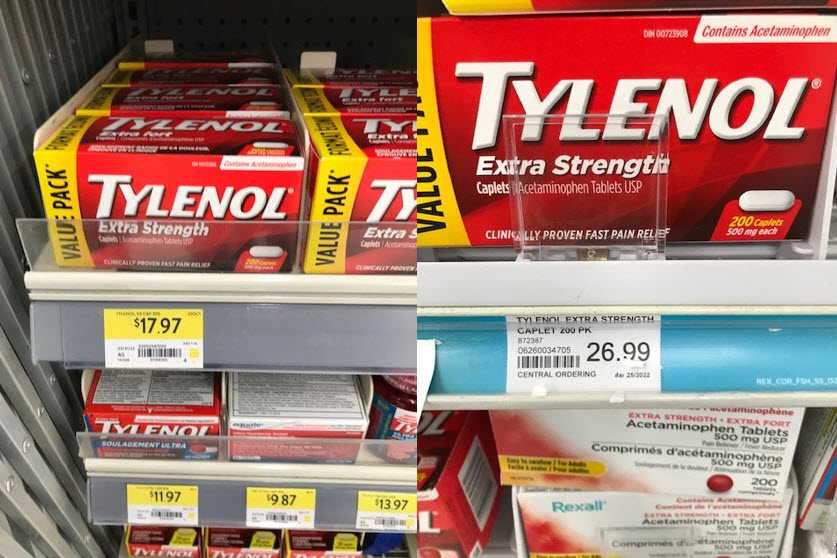

Other items have always been less expensive, but brand-name companies know how loyal we are. Here’s a great example: I was loitering in the pharmacy area of Walmart two weeks ago waiting for a prescription. At the end of the aisle (companies pay for that prime spot) was a sale on Tylenol.

Costco 390 tablets for $22.99 = $0.059 per

While I stood there for about 10 minutes, at least a half dozen people walked by and grabbed one of the packages. Yet, right beside these, just not on the end-aisle were the no-name acetaminophen. Same product without the brand name!

Costco Kirkland Acetaminophen 500 tablets down to $0.016 per

They’re almost 350% cheaper! Yet nobody reached the two feet further to save three and a half times the money! No, that wasn’t very scientific, but it sure got me wondering where else we buy something blindly because of loyalty instead of checking the price!

For comparison, assuming it has to be Tylenol for some specific reason, here are the Walmart and Rexall prices from the same day:

Walmart 200 pack at $0.09 per Rexall 200 pack at $.135 per

While not everyone has a Costco membership, their no-name at 1.6 cents per compared to Rexall at over 8 times as much is a reason to re-think your brand loyalty, to shop around, and to consider a Costco membership (because half of it would have been paid for with this one purchase).

One thing is certain: Most of us shop at Walmart or Amazon at least once a month or (a lot) more. One is pretty convenient to get to and one is just a few clicks away on your phone. Which one you drive to or click on is becoming more important to your wallet. Because, if you don’t comparison shop, it’s going to empty your wallet rather quickly.

From its inception, the goal of Amazon was to dominate the market with low prices. But that ended, or rather it transitioned, to convenience quite some time ago. With a reported 100 million plus people having Amazon Prime, there is an entire generation that values the convenience of two clicks to buy and guaranteed next day delivery. Amazon is banking on the fact that those prime customers don’t shop around much – and they’re right.

Convenience trumps price – just like the closest ATM with a four dollar “service” charge trumps free withdrawals at our own bank three blocks down the street. As we’ve talked about more than three years ago, Amazon isn’t the least expensive on identical products almost half the time (according to studies originally reported by US consumer guru Clark Howard.

Walmart also has some weird pricing on their website. Most of it appears to be from third-party vendors (which is also the vast majority of Amazon’s inventory. Here are some of my shopping attempts and price comparisons from the last two weeks:

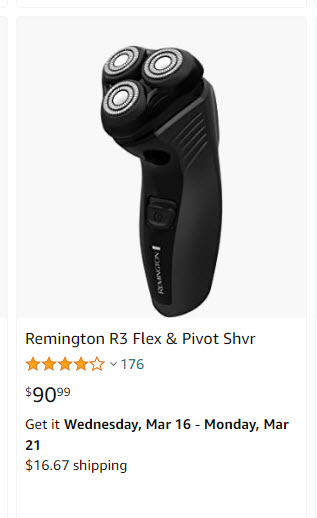

Yesterday I bought the pretty plain Remington R3 razor at my local Walmart. I thought $40 was a little high, but bought it anyway…until I got home and checked Amazon! $118 total vs. $40 is insane!

The legal rip-offs for those not bargain shopping works the other way around, too. This is a simple 10 pack of plastic cover plates for light switches: $15 from Amazon vs. $64 from Walmart for a 12-pack!

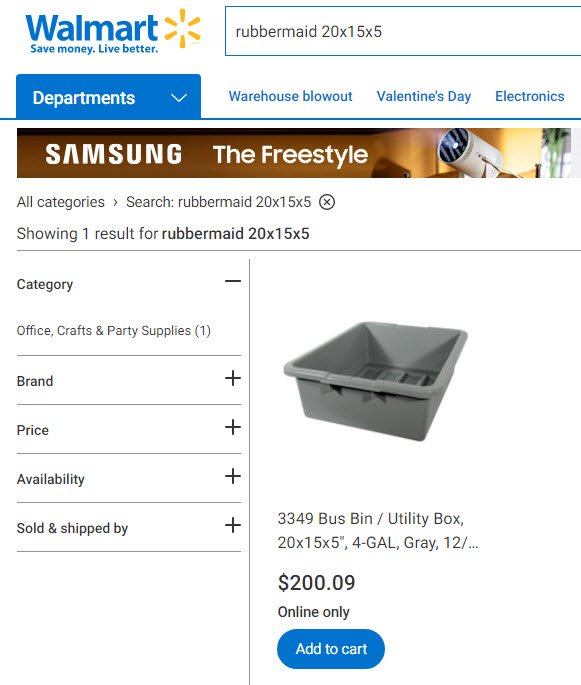

A gray bus pan that restaurants use to clear tables: I needed two of them since they’re great for the garage. But I almost had a heart attack seeing the Walmart price of $200…for something I bought at Costo Business Centre for $6.

There were a few more of my purchases – or purchase attempts – from the last few weeks where either Amazon or Walmart weren’t even close. While these may be obvious, it’s the 20 smaller things you buy where the prices are “only” out 10 to 20 percent that don’t make it onto our “better double check that price” radar. And that’s what both of these giants, and their third-party vendors count on. At a time when it seems like everything is already up in price by at least 10-20 percent, take the two minutes to compare prices. Your wallet will thank you!

Since you can buy pretty much everything at Walmart, why not a used car? Yes, Walmart is now in the car business. It started last year in the U.S. with 14 locations in Dallas, Houston and Phoenix and went so well, it’s now rolled out to 250 stores. It’s called Carsaver and lets you buy at an instore kiosk, a downloaded app or a dedicated website at carsaver.com

Walmart’s Carsaver doesn’t actually compete with used car dealers since you take delivery at the dealership. But they do claim to save buyers $3,500 and another $3,900 with their lifetime no mileage restriction powertrain warranty. Let’s hope that something else that starts in the U.S. and does come to Canada.

I was inspired: On December 7th, someone walked into the Walmart in Bedford, Pennsylvania and dropped off a bank draft for $46,265. It was an anonymous Christmas present in paying off 194 layaways at the store. Clearly, layaways are done by people who can’t afford to pay the full balance of something at the time and thus pay it in small installments before taking possession. It’s not the first time this person has done it, and sure made the Christmas of 194 people.

I messed up: We all know better, but make the number one rookie financial mistake, so I’m not alone. I was in a national retailer last week and saw AAA batteries on sale at 50% off. Half price for a package of 10. I grabbed them, paid, and left. The next day I was at Home Depot and saw the same brand of AAA batteries at the same sale price, but a package of 48 and not 10! YIKES. The first chain’s 50% off may have been legit, but they were still charging 480% more than Home Depot! How often do we look at the 50% off sign and buy without having a clue if it’s a good price or not! I did return the first ones, but it was a good lesson to learn over and over again: It’s the price you pay, not the discount you think you’re getting!

I was surprised by a survey last week that found 63% of us admit to re-gifting something. I think it’s probably way higher, but at least a lot of us are prepared to admit it. I’m in that group and there’s nothing wrong with that. If it’s a gift that you don’t need or want, it’s new, and it’s something another person would really enjoy, why not? Plan B would be to throw your gift out or give it to the thrift store and then buy the same thing again at retail price? That’d just be dumb…

And my big idea for the week will work great if you have young kids. Change one of the names of your friends in your phone to read Santa. Then have the person send you the odd text asking how the kids are behaving. I bet it’ll work like a charm…maybe even year round…

Walmart, the worlds’ largest retailer announced last week that they’re kicking out Visa in Canada. But I doubt that’ll happen.

Walmart claims they pay over $100 million in merchant discount fees. Those are the fees charged by credit card issuers when you use your credit card for payment. These amount of these fees depends on how much business a retailer does on credit cards. With MasterCard, for example, it’s as low as 1.26% when there’s $3 billion in business a year. Mine, on the tiny business side is 2.75% with Square.

There are over 72 million Visa and MasterCards in Canada, according to the Canadian Bankers Association. Ballpark, 60% are Visa cards, so I doubt this will come to pass. I just can’t see it happening. The average credit card charge in Canada is $103 and the typical Walmart customer isn’t likely to just switch to using their debit card, instead. The “no more Visa” plan is supposed to start rolling out July 18th in Thunder Bay. OK, they didn’t exactly pick the city with the largest volume business in the country. And they made it effective six weeks out. That means we’ll just have to see who blinks first: Visa in lowering the fees for Walmart, or the retailer in realizing this isn’t a winning idea.

In Miami, I recently saw the future of Best Buy, if they do survive. It was in a mall and they called it Best Buy Mobile. The store was about the same size as a typical cell phone store in every mall: Displays down both sides and a counter at the back. All the apple and phone products, ear buds, and the 90% of gadget stuff that fits into your hand. No more 35,000 square feet stores…

Singer Nicki Minaj recently had her social security number hacked and posted online. The rapper’s credit score dropped over 100 points almost immediately with a wave of inquiries into her credit report. Your credit score sets your borrowing interest rates. If you apply for credit at a bunch of places for different things, it’ll drop your score a lot and then your current line of credit or credit card rates may go up as a result.

At least some of the banks aren’t playing the delay game anymore with making online bill payments. They used to take two or three days to forward the money to the company you were paying. But recently I made a payment to Amex one night and had their email confirmation of receipt before 8 AM the next morning. Now if they could just cut down the average two weeks time it takes them to transfer out investments and RRSPs!

Walmart is the world’s largest retailer. When you’re that big, you measure efficiencies in pennies and seconds. I was in the U.S. recently and had my credit card out while the cashier was still ringing up my purchases. She told me to swipe my card. But she hadn’t rung everything through! I didn’t matter. In order to avoid the two or three seconds it takes to make the connection and get the approval on the credit card, their system does the connecting before they have the total amount. When the cashier hits the total button, the system just needs to match the amount without the wait for the swipe and connection. Yes, to Walmart – seconds matter at millions of transactions an hour.

Considering buying an electric car? If so, hold off. I hadn’t considered that a few years ago, there was a huge wave of leases to boost sales. Those leases expire next year so you’ll be able to get an incredibly great deal on a three-year old!

And the best ‘I didn’t know” has to be the stupidity level of some crooks.In Jacksonville, Florida, a crook went into a bank to cash a cheque for $368 billion. Yes – billion! Imagine his surprise when they called the cops, instead of handing him maybe a hundred suitcases of cash…

Do you want a way to guarantee you’ll get the lowest price on whatever you buy?

There are now a number of apps called showrooming…but for the U.S. only right now, and that comparison won’t help you, but only frustrate you.

The perception or reality is that Walmart isn’t considered the lowest price retailer anymore, and that’s something they want to correct! In nine cities they’re now testing something called Savings Catcher. You just need to enter your receipt number online. Just the receipt tracks everything you’ve purchased anyway. If Walmart finds another retailer with a lower price, they’ll immediately refund the difference to your credit card. Unless you live in San Diego, Dallas, or one of the other seven test cities, you’ll have to wait quite a while to sign up for it, though.

Should your credit rating be partially determined by who is your friend on Facebook or on LinkedIn? Another lending site called cabbage has now started using social media to determine your credit score. Yes, who you have as friends on Facebook can impact whether you get a loan or not. In the old days, your banker used to know you – character was a part of the decision making processing. These online lending sites have found that the chance of someone going past due is reduced 20% with a good social media score. It sounds wrong and stupid, but they think it matters and works. So somewhere down the road – be careful who you friend on Facebook.