Instead of putting their product on sale, Pizza 73 is advertising limited edition (Edmonton) Oilers game box pizza. If you’ve ever wanted to collect used greasy pizza boxes, don’t miss this promo!

Twice last week someone asked me when governments will be back to some kind of balanced budgets. Being asked that is very rare – it’s not something that most of us do as individuals. Hands up if you even do some kind of budget… Hands up if you remember any talk about that in the last two elections? There wasn’t anything. But many remember Prime Minister Trudeau’s comment that “budgets balance themselves.” Besides, running deficits allows politicians to buy votes. Getting to balanced budgets costs them votes!

Middle of January I saw a Royal Bank ad promoting investment accounts for RRSP season. The “deal” was that you get 100 free trades until March 31st. If you need more than two or three trades in the first two months, you’re doing something wrong! You’re not a day trader, I hope, because 93% of them lose money. I manage a 7 figure investment account for a relative. It’s with a national portfolio manager in five accounts. Last year they did a total of 16 transactions. That’s three per account in a year! 100 trades should last you more than 30 years…if you’re investing and not churning, guessing, or day trading.

Wow, you’d think that after 15 years and almost 700 of our radio segments we’d have talked about everything by now. Not true – not even close – never in the world of money and finance!

Pop quiz: Is hiring a company for a $20,000 job to finish your basement considered a home improvement? Nope – probably not.

Is buying gum and hand cream at Lowe’s considered a home improvement purchase? Yup.

See – and you thought you knew!

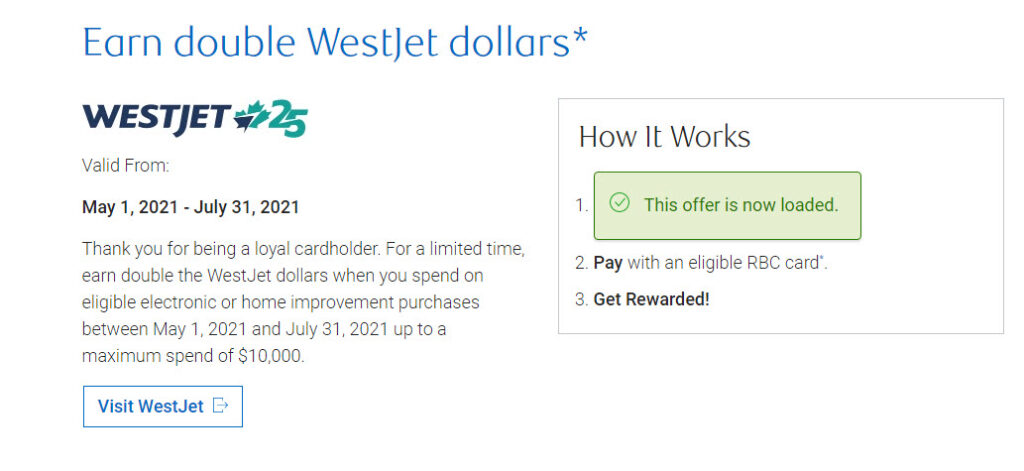

On Monday, the Royal Bank Westjet MasterCard (MC) started a double points (Westjet dollars) promotion on “eligible” electronics and home improvement purchases. Just after I bought $200 of treated lumber – it never fails…

Almost every card will have these promotions from time to time. But it’s buyer beware because the key word is “eligible” purchases. The hundreds of thousands of retailers and companies who accept credit cards all have a merchant category code (MCC) that identifies their primary type of business. My company is consulting – so it’s coded as professional services. That’s the same for accountants, dentists and the likes. So if you buy some lumber from your lawyer, or an “I love George Wednesday mornings” T-shirt, it’s still a charge in the category of professional services and not home improvements or clothing.

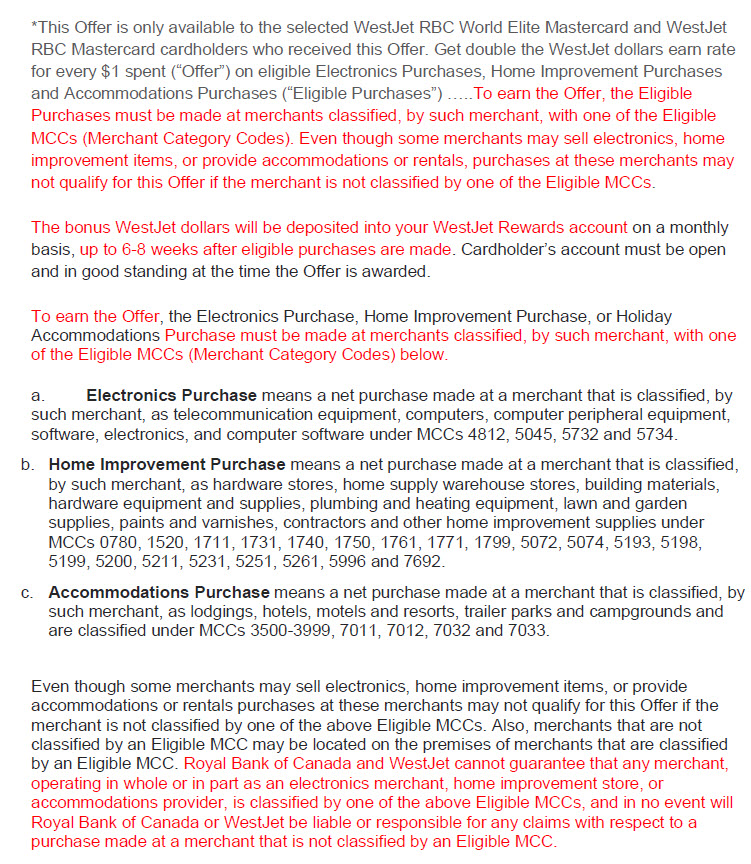

It is not what you buy that matters. It’s a charge in the right category that determines whether you get your bonus points for any promotion. A contractor won’t be coded correctly so your $20,000 charge won’t get you bonus points. But Home Depot, Lowe’s, Rona, Home Hardware, General Paint, or the likes are always coded home improvements. So whether you buy gum, lumber, paint, or appliances there, you’ll get the points.

Here is the full disclosure on the bonus point offer. It took me almost half an hour and comes from three different places. Thank you Royal for the details, but would you look a half hour to find these when your card offers them?

-Your bonus points won’t show up on your statement for 6 to 8 weeks. By that time, any promotion is probably over and you won’t know if you actually got them.

-You can’t get the MCC code in advance to know if you’re buying the right stuff from the right merchant with the right code.

If you stick to the “obvious” retailers, you’re safe – but never sure. Here’s the disclosure. It’s the same for every points promotion but I bet you’ve never heard of seen it:

Home Improvement Purchase means a net purchase made at a merchant that is classified, by such merchant, as hardware stores, home supply warehouse stores, building materials, hardware equipment and supplies, plumbing and heating equipment, lawn and garden supplies, paints and varnishes, contractors and other home improvement supplies under MCCs 0780, 1520, 1711, 1731, 1740, 1750, 1761, 1771, 1799, 5072, 5074, 5193, 5198, 5199, 5200, 5211, 5231, 5251, 5261, 5996 and 7692.

Costco is considered a discount club with MCC5300 –Walmart is typically MCC5310 (discount store) or MCC5311 (department store) but they may also have a code set up under MCC5541 (groceries) – but that’s unlikely. So no bonus points there for any promotion from anyone – ever.

You could:

-Call your card issuer and ask for the MCC code for a specific retailer – but I doubt you’d get it.

-Check your old statements in case they’ve had the same promotion in the past where you can see what qualified.

-If you get an annual summary of charges (not with Royal Westjet) that will give you the spending under specific categories and you’ll be sure those stores qualify

Or do what most everyone does: Get excited about the promotion and charge away and hope you might get the points in the MCC code crap shoot.

Lastly, if any bonus offer ever has you buying from a more expensive retailer just to get the points, you’re tripping over dime to pick up a penny. You REALLY need to read the “what are your points really worth” on page 139 of the Money Tools book.

Banks

started offering payment deferrals about a month ago, and it’s now over half a

million who have done so – and that’s just mortgage payments. But there may be

a problem, especially for the early applicants: It may have destroyed your

credit rating.

But

let’s back up a minute first. There are two credit bureaus in Canada. TransUnion

and Equifax. Unfortunately Equifax has 90% of the business and is the primary

source for almost everyone but Scotia. They’re just a really horrible company

for lots of reasons. But both credit bureaus, when the thought of extensions

started immediately called on the banks to set up the correct coding for these

extensions. But the banks were slow to get this done.

If

our listeners had only a one number code to rate the segment, it might be 1 for

great, 2 for boring, 3 for make George go away, or 4 for average. That’s it –

four codes. That’s how the credit bureau does things. But a deferral didn’t

have a code set up. So a ton of the first deferrals went through as unpaid –

which means behind in payments – which means a huge drop in your credit score

until the banks reported the deferrals with a new code.

The

how to check your files is in the credit burau chapter of the Money Tools book.

Just go online to Mosaic or yourmoneybook.com if you don’t have a copy.

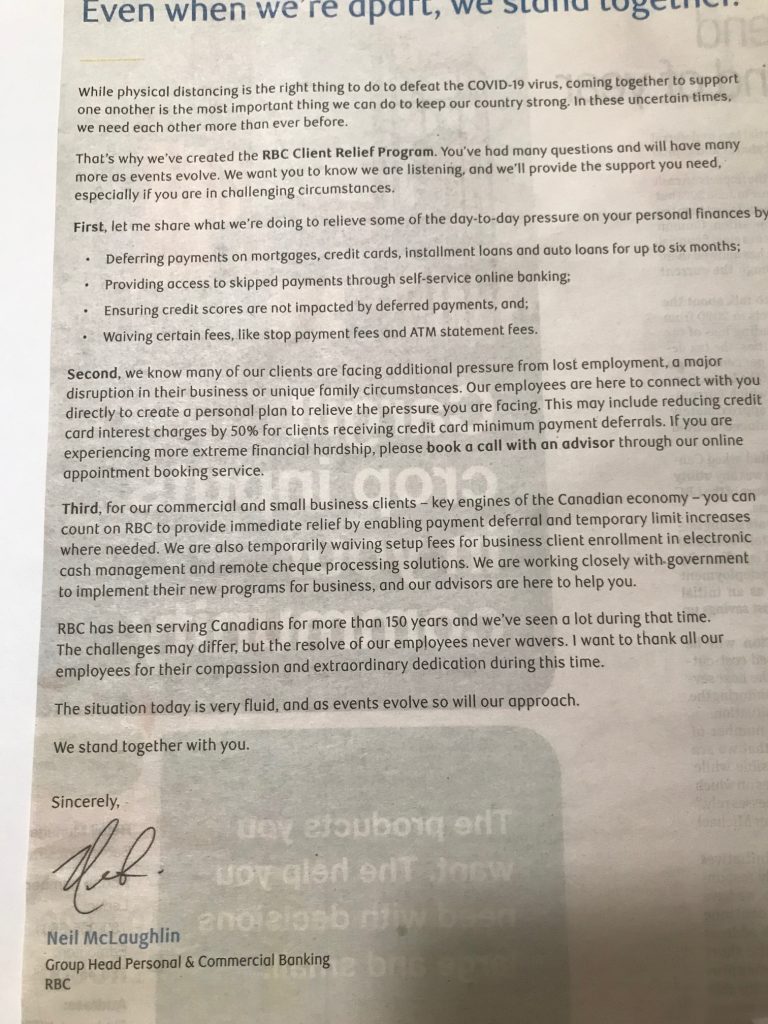

If you’re impacted, it’s obvious that you need to get this corrected – and that could be a part-time job. If you deal with the Royal, their Canadian President had an ad in newspapers across Canada the first week in April. In there, it stated that they will “ensure credit scores are not impacted by deferred payments.” Here is the full ad:

If

yours was, here is the contact information for the President who wrote the ad:

Neil McLaughlin, Group Head – Personal & Commercial Banking 200 Bay Street, PO Box 1, Royal Bank Plaza Toronto, ON M5J 2J5 Phone: 888 212 5533 (your odds are zero of even reaching his EA, though and you want your issue in writing anyway) Fax: 416 955 7800

If

your credit report problem is not with the Royal, you’ll need to do some online

searches for their head office and/or a Regional VP and an address.

And

here is a form letter that you can use. Search under radio stories to get the

information on how to complain effectively that we talked about a few months

ago. Keep it simple, keep it short, factual, and state what you want to

achieve. And always always keep every copy of every letter or email and a

record of every call and the time, date and who you spoke to. This is too

critical not to be disciplined!

If

you don’t deal with the Royal, you can use the same letter, just take out the section

referencing their advertisement.

Dear

Sir:

Re:

Incorrect credit reporting of my deferral

Your

bank processed a deferral of my (mortgage/credit card/line of credit/loan)

payment in the month of xxx.

However,

my credit report since that deferral shows it reported by your bank as past

due. That is NOT correct and has to be corrected. As you know, this has a huge

impact on everything from my insurance to interest rates and future borrowing! As

you also know, the credit bureaus (TransUnion and Equifax) cannot fix this

error as (you) the lender has to submit the right reporting information to

them.

Your

national advertisement the first week in April, under your signature, stated

that you were “ensuring credit scores are not impacted by deferred payments…”

I

need to have someone in your office correct the coding from the incorrect “past

due” to the corrected “deferral,” and re-report it to the credit bureaus.

Or

in the alternate supply me with the proper person, their address, and/or email

in your bank that I need to contact to get this corrected immediately.

I

look forward to hearing back from you – thank you in advance,

Yours

truly,

(Your

name)

Address:

Telephone

#:

Branch

you deal with and main account #:

Account

# of deferred credit card, loan, line of credit or mortgage

AND

send or deliver a cc copy of this letter to your branch as well!

Researchers at Newcastle University found that criminals can hack your Visa card in less than 10 seconds. All they have is your card number and what they’re missing is the three digit security code and the expiry date.

With just a laptop and a simple computer program, they run all the possible combinations of your security code and the expiry. In just a few seconds they have all the information they need to start shopping online.

It only works with Visa who doesn’t have a blocking system when multiple tries are made with your card. MasterCard and Amex block the criminal after just a few incorrect attempts. Now don’t panic. You’re never liable if your card is misused – ever! But wouldn’t you think Visa would care about absorbing millions of dollars in fraudulent charges?

If you’re turning 60 or 65 this year, write a note on your calendar: You’ll be able to get much of your banking service charges stopped! Credit unions are at age 60, but you’ll have to check with your specific bank if they’re at 60 or 65. I do know the Royal is now age 65 as they just changed it. Ah, how to legally rip off tens of thousands of seniors for millions of dollars…it’s detailed in the Money Tools book in the banking chapter.

It hasn’t been a good month for two of our banks. They couldn’t control the drop in their share prices after the vote in Britain to leave the European Union, but the other problems are purely of their making.

I wanted to share both last week, but since then, both have now become international news stories:

TD got their foothold in the U.S. during the financial meltdown. They purchased Harris Bank and another one called Commerce Bank. Commerce Bank was loved by their customers. But those same customers might not be loving TD right now. NBC did an investigative report into coin counter machines. TD was found to shortchange people by 15% on their coins.

What? A bank that cannot count? Not a good PR move! On the other hand, you’d think the ones in retail stores might be questionable…but that’s not the case: They were all found to be accurate. Clark Howard, on over 400 radio stations in the U.S. calls it a big rip-off alert. Then it got worse: They knew their machines were ripping people off and STILL rolled them out in Canada! That’s now a class action lawsuit, according to CBC Marketplace. But when they knew this, why isn’t it criminal fraud?

The second one involves the Royal. Scotia closed most of their retail banking in the Caribbean last year. Now the Royal announced new and increased service charges for their customers. Some of them up to $11.75 a month. In the seven countries where they operate, the average minimum wage is $4.23. There have now been international media reports of lineups ranging two to three hours this week as locals close their accounts. That’s great to see: People voting with their wallets and firing their bank! Love it!

For years, jewelry stores have been envious of the “cash in your gold” places. The places that buy your gold will pay you 10 to 15% of the total gold value, according to Consumer Report. That’s a massive profit and jewelry stores weren’t in on it. That’s now changed, and Ben Moss was one of the first. They’ll also buy your unloved and unwanted gold. But they also run a jewelry store, which is some of the highest markup in retail. If you sell your gold at Ben Moss, they’ll give you 10% extra if you get it on a giftcard and not in cash. That way you’ve locked yourself into buying from them. And if you’re prepared to buy from them the day you sell your gold, they’ll give you 20% extra. But that doesn’t make it a better deal! You’re getting around 10% of the value and now buying something with massive markups and no chance to shop around because you have to buy today – and from them!

When was the last time you received a 40% raise? I didn’t think so: Yet, the CEO of the Royal Bank just got that after one year on the job. If you ever wonder what happens to the twice annual increases in your service charges, they go to pay the guy $11 million a year!

If you have an iPhone, an Apple error 53 is something you should remember. Stuff happens with your phone: The most common repair for people…mostly younger people…is to replace a cracked screen. Any repairs on an iPhone that are not done by Apple, at Apple prices, will trigger this error 53 and disable your phone. Sick, wrong, but true: Apple is forcing you to pay their full sticker price for repairs and will hold you hostage if you don’t. That ought to be illegal since you paid for the phone, aren’t asking Apple for warranty, and should be able to choose where to repair it. In most cases, that’ll be at half to a third of the Apple price. But it’s legal and now you’ve been warned. Don’t hold your breath for the government to make that illegal. They should, but they won’t.

According to PIAC, we already pay over $700 million in paper statement fees in North America. And, since it’s summer again, it’s the bi-annual increase in service charges. Global Television had a big story on the Royal leading the way with their 18 million customers.

Have we just become numb to this, shrug our shoulders, and take it…twice a year? That’d be sad, but I have a hunch that that’s the case. The nastiest change by the Royal is that the seniors fee plans are changing from age 60 to 65. Great if you’re a shareholder because you get to rip off millions of seniors for another five years. That’s 60 more months of full service charges! The story featured one lady who has set up an appointment at her branch to see if she can get some fees waived. Sorry, lady – you’re wasting your time. The quote from the Royal was “we’re working hard to keep costs down.” That’s funnier than any comedy show you’ll watch this year.

What’s the behind the scenes reasoning for this one? We Canadians are slowing our borrowing down a bit. Maybe not by choice, but because we’re pretty maxed out. It’s also the result of a slower economy. Do you think banks are just going to see their income drop from interest income and not replace it somewhere else? The Royal already makes $1.5 billion in account service charges (2014). That’s 5% of all their income! Want to bet it’ll hit $2 billion this year if you don’t go somewhere else?

Why can the banks do this? Because they’ve made millions of you really sticky. That’s a bank phrase that they focus on a lot. When you’re stuck – you don’t move elsewhere. If you have five dealings with a bank you’re so stuck, you’re not moving. A chequing account, direct payroll deposit, some RRSPs, a credit card, maybe a line of credit, and a mortgage, and they’ll likely have you forever! Then you’ll pay the increasing service charges, whatever fees they dream up, and take whatever bad service (if any) that you can get.

You’ll complain and moan. but you ain’t moving to a credit union. Your perception is that it’s too hard to move everything. It’s not! Get to a credit union TODAY. Open a chequing account and change your direct deposit. That’s the big step: Where your income is going. Then move your auto payments and you’re set. Oh, and while you’re there open up a Choice Rewards MasterCard, low-rate, or student card. No fees, no hassle, better and more flexible rewards, getting treated like an owner (because you are), and you’re never going to be charged a fee to enter a branch, or to pay your own payments down the road. It takes an hour of pain to move things around…for a lifetime of being valued for your business AND a rebate the end of year on all your dealings! My service charged went DOWN this month AND I got over $600 back in my annual profit sharing! As Nike says: Just Do It! Enough is enough! The government isn’t coming to help you here – so repeat after me: If it is to be – it’s up to me!

But part two is even nastier. The Royal announced they were thinking of charging their customers to pay their own Royal Visa payments, their loan payments, and mortgages. Yes, you heard that right. A service charge to pay payments for their own loans and credit cards. Last Friday they backed off. But you have to know this will come up again. How sick, sad, and just wrong!

The Federal Government has a long track record of not being big on helping consumers. They did force cell carriers to discontinue their paper statement fee. Yet they aren’t shutting down the banks from these rip-off fees that are probably a hundred times more than the little cell carriers and impact millions more people. Is it because Bay Street and the big no-service banks are some of the biggest contributors? You decide…

f you have a Best Buy Visa card – you need to pay attention. Best Buy (that includes Future Shop as they own them) has announced that they’re cutting long time ties with Chase for their Reward Zone Visa. They’re switching their credit cards to Desjardins, a Quebec based credit union, in April joining the Source, Rona, Staples and others…

Because they’re switching carriers, Best Buy announced their credit card will be deactivated the end of February. You’re not automatically getting a Desjardin Visa card because they’re different companies. You’d have to apply all over again if you want the new card.

That will drop your credit score and credit rating! The card will now go to a zero limit since it’s deactivated. THE biggest part of your credit score is the percentage of limits versus balances! Your total credit card balances need to be below 30% of your total limits or your score starts dropping. If you owe more than 50% of your limits, it’ll plummet. If that applies to you, you HAVE to apply for any other Visa or MasterCard BEFORE the end of February – before your credit score drops. You should have two or three major credit cards owing less than 30% of your limits! Do the math and email me if you don’t understand the math or the trouble that could be coming your way thanks to Best Buy.

The same thing applies to bankrupt Target in Canada. Their Visa is through Royal Bank. No more Target means no more Target Visa. Before it’s terminated on you and the corresponding credit limit removed, you’ll need to replace that limit. If you choose to stay with the Royal, call them and it’ll be a simple swap to another card. If not, you need to apply somewhere else online.

Do remember that you need to get or keep your percentage owing to less than 30% of your limits. If you regularly pay off, or pay down, your cards, and already have two major credit cards – you don’t need to worry!

Canadian banks are kind of ashamed they’re Canadian. Bank of Nova Scotia is now Scotiabank, Toronto Dominion is TD, Canadian Imperial Bank of Commerce has been CIBC for a long time, and the Bank of Montreal is BMO.

Last week, the Royal Bank went on a huge wave across the country to replace all their branch signs to read: RBC Royal Bank. The next wave will be to do away with the Royal Bank part altogether. Oh how I want to be in the sign business. In Canada it’s cool to be Canadian, but in the rest of the world, they don’t want to advertise that at all.

The RCMP in BC want to get the word out on a new phone/credit card scam. The crooks already have your stolen credit card number and give you a lot of information to put you at ease. All they’re after is the three digit security code and they can go crazy with online purchases. It’s the last and only thing they ask for, claiming they just need to “verify that you’re the cardholder.” Don’t ever talk to anyone about your credit card. Hang up the phone and dial only the number on the back of your card! Here’s the link from the RCMP:

Last week, CBC’s Marketplace did a short story on breakfast sandwiches. They’re loaded with fat, get you two-thirds of the daily sodium and a ton of calories. But here’s an alternative diet plan: Last week, New Hampshire just rolled out new scratch and win lottery tickets. They are now bacon flavoured. So grab your coffee and just sniff the lottery ticket. You’ll still lose, but you’ll win on the calories, fat, and sodium reduced breakfast!

Also last week, TD rolled out a ton more new ATM machines. These ones are optical readers. Just insert the cheque or cash you’re depositing. No more envelopes and you don’t even need to key in the amount of the cheque. Your receipt will print out a picture of the cheque you deposited. It was only last year we talked about taking a picture of a cheque with your smartphone and it’s deposited. Boy, how technology is advancing quickly.

The middle of last week, the Bank of Canada cut the bank rate by a quarter of a point. We’re a resource country and they’re seriously concerned with our economy with oil dropping by almost 50%. Within 24-hours, the banks cut most of their savings accounts interest rates by a quarter point. But they also announced that, no – they’re not cutting their lending or mortgage rates. So savers get ripped off and borrowers get hosed in order to make another few billion dollars. NOT nice and not right!

OK, if that doesn’t sound like great news – you’re right. But this Ipos Reid survey was done for the Royal Bank. Not to pick on the Royal, but banks are in the business of helping you go broke. They’re in the lending business and generate their profits when YOU borrow money and pay interest. So it is great news…if you’re a lender.

For the rest of us: Not so much. A 21% increase in just the last year of our non-mortgage debt is insane. That’s the Canadian average, but Alberta set the record with a 63% increase in debt last year. With pretty good incomes in Alberta and elsewhere comes that part of the brain that says: It’s OK, just borrow the money – you make enough to pay it off…eventually.

The survey also found that the same 38% of us are “very anxious” about out debt level as those who responded they’re “comfortable” owing the money. If you’re in the “comfortable” group, what would move you out of that? A job loss, any emergency, your partner leaving their job, the need for a newer vehicle, or a host of things that can go off the rails. Don’t get too comfortable, because things can change in a hurry – and it’s always when you least expect it.

When interest rates are low we tend to think we’re getting free money. Well, they won’t stay low forever, and when they turn, the interest you’ll pay goes way up for something you spent years ago. There’s a current radio ad with the line: You can eat whatever you want and still lose the weight. In financial terms, it’s just as much nonsense, but I bet most of us believe it – or at least want to believe it: You can borrow and spend whatever you want and still be financially successful. No you can’t. You can’t spend more than you earn, and you can’t eat everything you want and still lose the weight. Oh how we’d love that to be true. And after all these decades of weight loss programs having a more than 90% failure rate it isn’t any different for our finances.

For the majority of us, we earn enough for what we need. But we’ll never earn enough for everything we want. And it’s the “wants” that kill our finances, choke us with monthly payments, and stop us from putting any serious money into retirement plans, or even a simple emergency fund.

Until we get real and stop buying into the ads and marketing we can’t turn our finances around. Sorry, it’s mathematically impossible. May the reality check of that hit most of us before it’s too late and before we’re in our 60s and have 20 minutes left before retirement to put some money way.

Or, if you can’t retire when you really wanted to, think back to all the credit card charges, all those vehicles you owned and sold for one-tenth of what you paid, and that line of credit that was around so long you started thinking it was a member of the family…